The 2026 non-USD stablecoin landscape

The non-USD stablecoin sector has reached a significant structural threshold. As of 2026, the circulating supply of stablecoins denominated in currencies other than the US dollar has surpassed $2 billion. This milestone represents a 42% year-over-year increase, marking a shift from experimental use cases to regulated infrastructure.

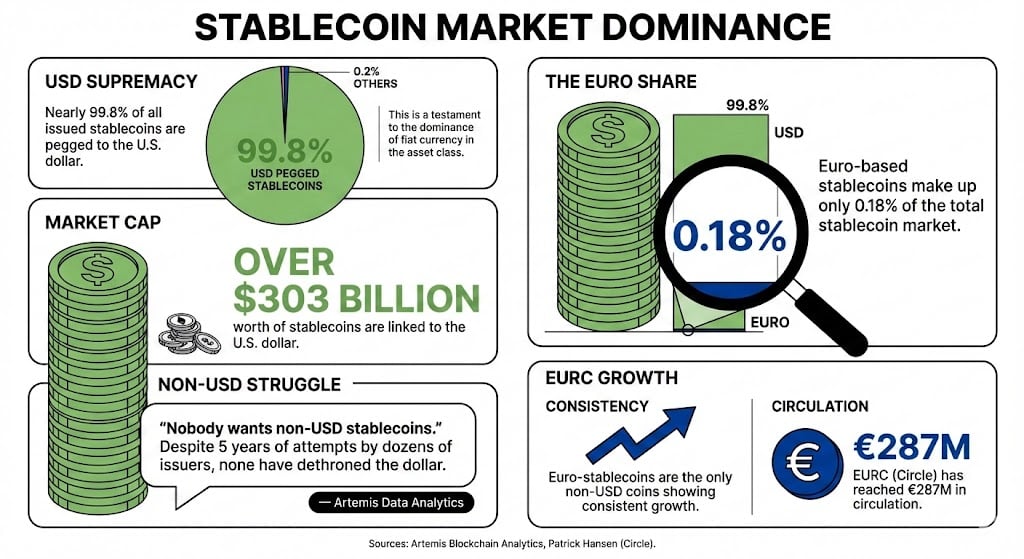

Despite this growth, the sector remains niche relative to the broader market. USD-denominated stablecoins continue to dominate trading and settlement volumes due to entrenched network effects. Non-USD tokens serve specific, context-dependent roles, primarily in regions where local fiat volatility or cross-border friction creates demand for alternative settlement layers.

Regulatory frameworks are now defining the viability of these assets. The European Union’s Markets in Crypto-Assets (MiCA) regulation, the UK Financial Conduct Authority (FCA) guidelines, and Japan’s Financial Services Agency (FSA) rules provide the legal scaffolding for EUR, GBP, and JPY stablecoins. These regimes emphasize reserve transparency and issuer licensing, moving the industry away from unregulated issuance toward compliant financial instruments.

The acceleration in 2026 is not merely a function of market speculation but of regulatory clarity. Institutions and retail users in the Eurozone, United Kingdom, and Japan are increasingly adopting these tokens for payments and savings, driven by the predictability offered by compliant issuers. This trend suggests that non-USD stablecoins are evolving into a permanent component of the digital payments landscape, even if they do not yet challenge the dollar’s global dominance.

European regulatory framework for euro stablecoins

The Markets in Crypto-Assets Regulation (MiCA) establishes the first comprehensive legal framework for stablecoins within the European Union. For issuers of euro-pegged tokens, known as Asset-Referenced Tokens (ARTs) or e-Money Tokens (EMTs), compliance is mandatory for market access. The regulation mandates strict reserve requirements and operational standards to ensure stability and protect holders.

Reserve requirements and asset segregation

MiCA requires issuers to hold reserves fully backed by high-quality liquid assets. These reserves must be segregated from the issuer’s own operational funds to prevent commingling. The assets must be held in custody by qualified third parties, ensuring that they are insulated from the issuer’s credit risk. This structure is designed to guarantee that token holders can redeem their assets at par value at any time.

Licensing and authorization

Issuers must obtain authorization from a national competent authority within an EU member state. This process involves rigorous scrutiny of the issuer’s governance, internal control mechanisms, and compliance procedures. Once authorized, the issuer benefits from a passporting right, allowing it to operate across the entire EU without seeking additional national licenses. This harmonized approach aims to reduce fragmentation and enhance consumer protection.

Implementation timeline

The phased implementation of MiCA sets clear deadlines for compliance. The general provisions of the regulation entered into force in December 2024, with full application expected by 2025. Issuers must align their operations with these deadlines to maintain legal status.

Key takeaways

- MiCA applies to all euro-pegged stablecoins offered in the EU.

- Reserves must be segregated and held in high-quality liquid assets.

- Authorization from a national authority is required for market access.

- Passporting rights allow cross-border operations within the EU.

For detailed guidance, refer to the official MiCA regulation text published by the European Union.

UK and Japanese stablecoin compliance paths

The United Kingdom and Japan have established distinct regulatory frameworks for non-USD stablecoins, reflecting different priorities in financial stability and consumer protection. Both jurisdictions require strict adherence to local licensing or registration, but the operational requirements for GBP and JPY stablecoin issuers differ significantly.

United Kingdom: FCA Oversight

The Financial Conduct Authority (FCA) regulates stablecoins used for payments under the Financial Services and Markets Act 2023. Issuers must be authorized as electronic money institutions or payment institutions. Key requirements include:

- Full reserve backing with assets held in segregated accounts.

- Regular audits and disclosure of reserve composition.

- Capital adequacy standards to ensure operational resilience.

The FCA does not currently approve stablecoins for broader investment purposes, limiting their use primarily to payment transactions within the UK jurisdiction.

Japan: FSA Registration

Japan’s Financial Services Agency (FSA) oversees stablecoins under the Payment Services Act. Issuers must register as Payment Service Providers and meet strict reserve requirements. The FSA mandates:

- 100% reserve backing with cash or deposits in Japanese banks.

- Monthly disclosure of reserve status to the FSA.

- Prohibition on issuing stablecoins that do not meet the 1:1 fiat peg requirement.

Japan’s framework emphasizes transparency and consumer protection, with regular inspections and penalties for non-compliance.

Comparative Analysis

The following table outlines the key differences between the UK and Japanese regulatory approaches for non-USD stablecoin issuers.

| Requirement | UK (FCA) | Japan (FSA) |

|---|---|---|

| Legal Basis | Financial Services and Markets Act 2023 | Payment Services Act |

| Reserve Backing | Full reserve, segregated accounts | 100% cash/deposit in Japanese banks |

| Disclosure | Regular audits and reserve composition | Monthly disclosure to FSA |

| Capital Standards | Capital adequacy for resilience | No specific capital adequacy stated |

| Use Case Limitation | Payments only, no investment use | Payments and remittances |

| Enforcement | Authorization revocation, fines | Registration revocation, penalties |

Integrating regional stables into DeFi protocols

Multi-currency stable maps are reshaping how DeFi protocols handle yield strategies and cross-border settlement. By integrating non-USD stablecoins, platforms can align liquidity with local currency demand, reducing foreign exchange friction. This integration requires strict adherence to regional regulatory frameworks, including the EU's MiCA, the UK's FCA guidelines, and Japan's FSA standards.

-

Verify issuer authorization under MiCA (EU), FCA (UK), or FSA (Japan)

-

Confirm reserve assets are held in segregated, audited accounts

-

Ensure smart contract audits cover multi-currency swap logic

-

Integrate with on-chain forex infrastructure for low-latency settlement

-

Monitor regulatory updates for changes in stablecoin classification

The integration of regional stablecoins is not merely a technical upgrade but a regulatory necessity. As Standard Chartered and Zodia Markets note, there is a significant gap between USD stablecoin dominance and the actual role of the dollar in global trade. Bridging this gap requires protocols to prioritize compliance and local infrastructure over speculative yield. This approach ensures long-term sustainability and aligns with the evolving legal landscape of digital assets.

Common questions about non-usd stablecoins

Data from market registries indicates that 97% of fiat-backed stablecoins are denominated in the US dollar Wikipedia. This dominance stems from the fact that stablecoins function primarily as settlement layers for global finance, which remains dollar-centric. Non-USD stablecoins serve specific regional liquidity needs rather than replacing the dollar for global settlement.

No comments yet. Be the first to share your thoughts!